How are mortgage interest rates determined?

Mortgage rates are determined by a number of factors based on both the individual borrower and the economy at the time of lending.

Factors that are based on the borrower include:

Credit score: Interest rates are lowest for borrowers with credit scores of 740 or higher. In our experience, borrowers with credit scores below 640 typically have much higher interest rates and fewer lending options.

Loan-to-value ratio: This is a measure of loan amount compared to the home’s value. If you make a $20,000 down payment on a $100,000 home, your mortgage will be $80,000. This means you’re borrowing 80% of the property’s value.

A loan-to-value ratio greater than 80% is typically considered high and represents a greater risk to the lender, which may increase your interest rate or increase the need for mortgage insurance. Mortgage insurance is an insurance policy that protects a mortgage lender or titleholder if the borrower defaults on payments, passes away, or is otherwise unable to meet the contractual obligations of the mortgage. It is important to note that this is insurance that protects the lender, not the borrower. In other words, you are paying an expense to protect the mortgage lender.

Certain lenders understand that many early-career doctors can’t provide a down payment and offer doctor mortgages. These physician loans don’t require a down payment and allow physicians the ability to buy a home earlier than they could with a conventional loan.

Other factors that affect your mortgage interest rate include:

Economic factors: Factors like inflation, rate of economic growth, the Federal Reserve’s monetary policy, the bond market and housing market conditions all have varying impacts on mortgage rates. Investopedia breaks down these five factors into greater detail.

How does mortgage prequalification work?

Mortgage prequalification gives you the ability to see how much a lender will offer to you when you begin searching for your dream home. During the prequalification process, a lender will provide you with an estimate of the loan amount you will be approved for.

It is recommended to complete prequalification before you make an offer on a house. This helps you determine the amount a lender will lend to you and if you are comfortable with the associated monthly payment. It also puts you in a much stronger position with a seller or against other offers on the same home.

What are the different types of mortgages?

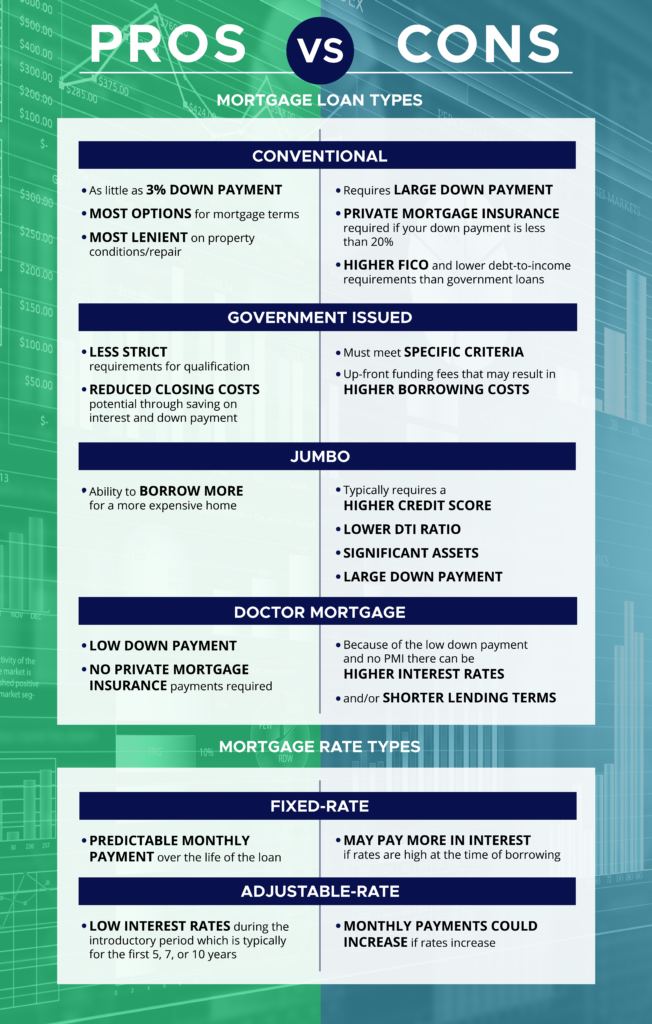

The three main types of mortgages are conventional, government or jumbo. Depending on the type, you may have a fixed or adjustable-rate loan.

- Conventional mortgages are the most common type of mortgage. These loans can have stricter credit score and debt-to-income (DTI) requirements.

- Government-issued loans are insured by government agencies and include FHA, USDA and VA loans. You may be able to qualify for a government-backed loan even if you can’t get a conventional loan as they generally allow for lower FICO requirements and higher debt-to-income limits.

- Jumbo loans are used for buying high-value property and can be more difficult to qualify for than other mortgage types. Jumbo loans are mortgage loan amounts that exceed the conforming loan limit for the area in which you wish to buy. (Most of the country has a conforming loan limit of $726,200 for a 1-unit property).

- Bonus: Doctor loans are mortgages built specifically for doctors — physicians, dentists and veterinarians. These loans have lower down payments that could help a doctor purchase a home before they would otherwise be able to.

- Fixed-rate loans offer a very predictable monthly payment because they have the same interest rate and principal-to-interest payment each month.

- Adjustable-rate loans have interest rates that change with market changes. You will have a fixed-rate for introductory period. After that period, if the market index increases, your rate will rise; if it decreases, your rate could lower. The amount that an adjustable rate, or ARM, could rise or fall depends on the floor, or ceiling of that mortgage loan.

FDIC-Insured – Backed by the full faith and credit of the U.S. Government

FDIC-Insured – Backed by the full faith and credit of the U.S. Government